HashKey Capital Monthly Insights Report: November 2025

HASHKEY CAPITAL

Reading Time: 11.61Min

HASHKEY CAPITAL

Reading Time: 11.61Min

Macro

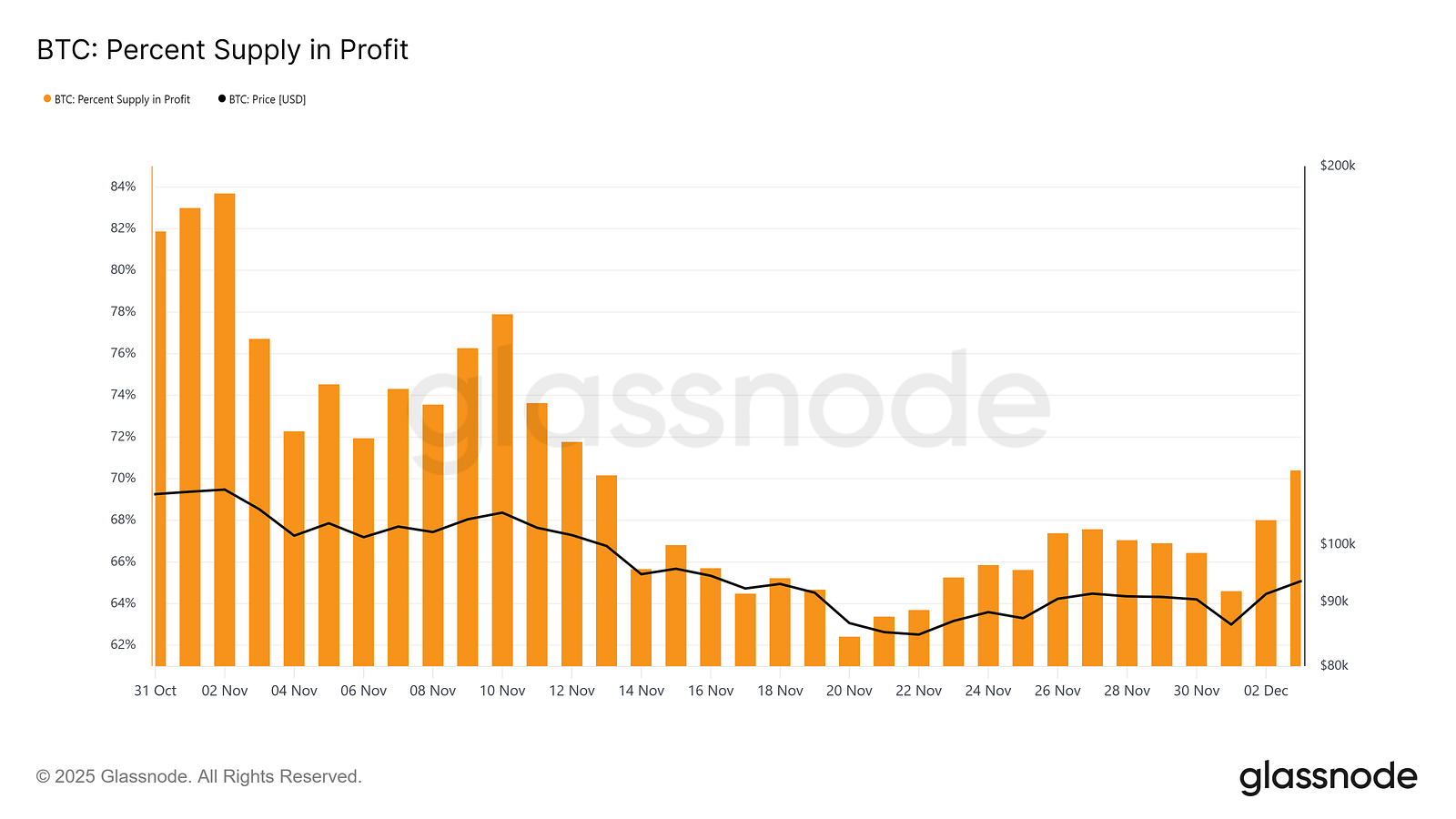

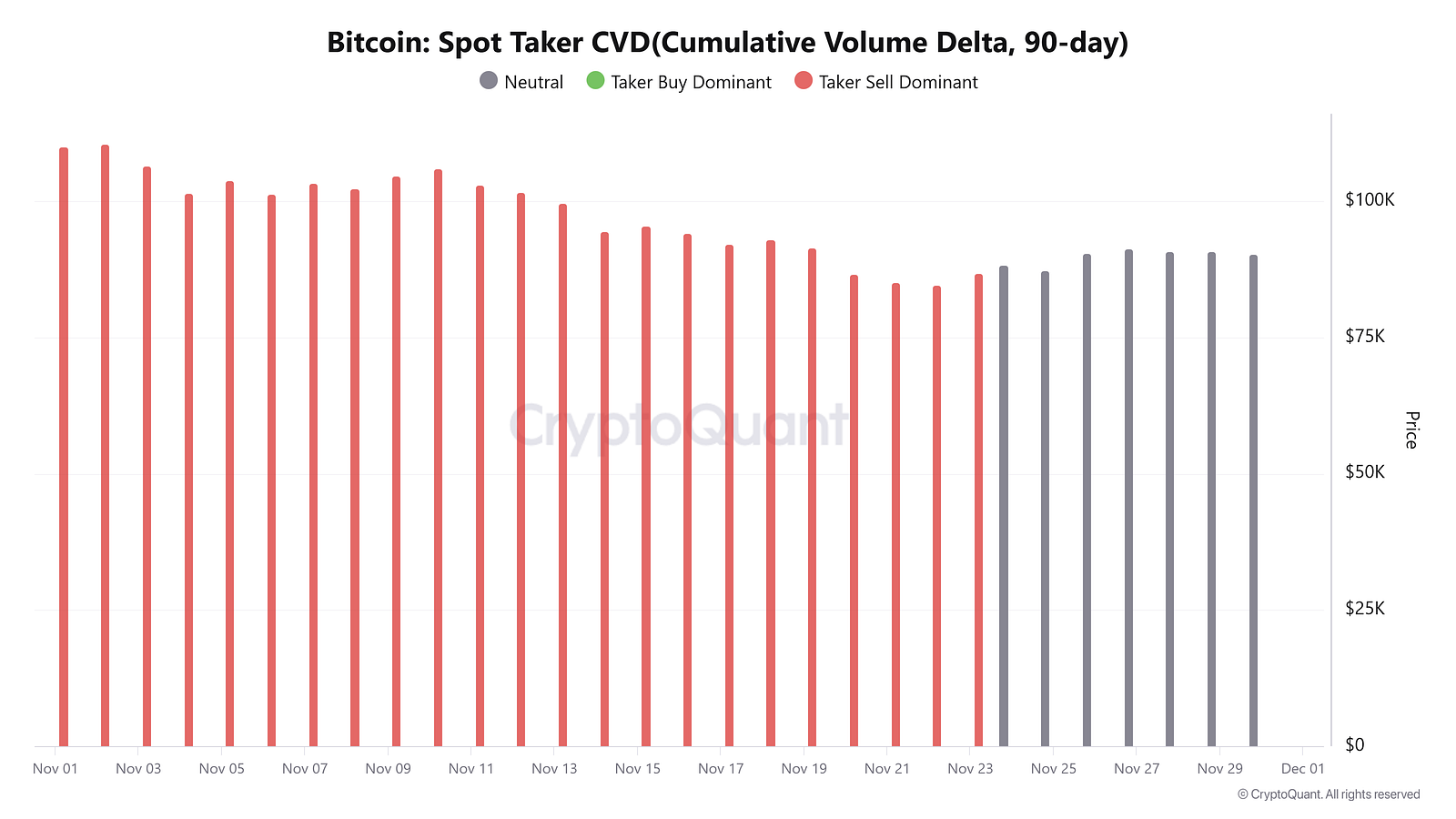

In November, crypto market sentiment further soured as more than $600B was wiped off the total market capitalization. The lack of regulatory catalysts, Fed rate cut concerns, correction in the valuation of tech and AI-adjacent stocks, as well as the repositioning of institutional capital have been key headwinds setting the dismal backdrop for November. Investors’ sentiment measured by the Fear and Greed Index reached 10 on 22 November, its worst level since the COVID drawdown, after $2B was liquidated on 21 November with most of the losses incurred by long positions. Bitcoin broke through a crucial $100K support level, plunging deeper down to $81,050 on November 21, dangerously close to another key support level at $80,000, and ended the month in bear market territory as it remains 28.37% off its all-time highs. Contrary to Bitcoin, gold’s safe haven status further solidified as it gained ~5% MoM, underscoring Bitcoin’s closer correlation to risk assets like Nasdaq which corrected ~3% led by losses in tech and AI heavyweights on overvaluation concerns. The decline in Bitcoin price has led to % of Bitcoin supply in profit declining from ~83% on 1 Nov to ~66% on 30 Nov. The Spot Cumulative Volume Delta(CVD), a metric that tracks spot BTC buying activity, has also remained in sellers’ territory for most part of November.

Beyond Bitcoin, Ethereum and altcoins have slumped in tandem. Aggregate open interests across major blue chip tokens have decreased by ~25% MoM, reinforcing risk-off sentiment as liquidity saps away in November.

Moving forward, Bitcoin price remains critical to watch — negative Fed rate surprises, delayed progress in US Market Structure Bill, lacklustre institutional appetite, and further recalibration in valuation of tech/AI names could further spook investors. On the flip side, positive developments in these areas could push Bitcoin above $100K again.

Bitcoin

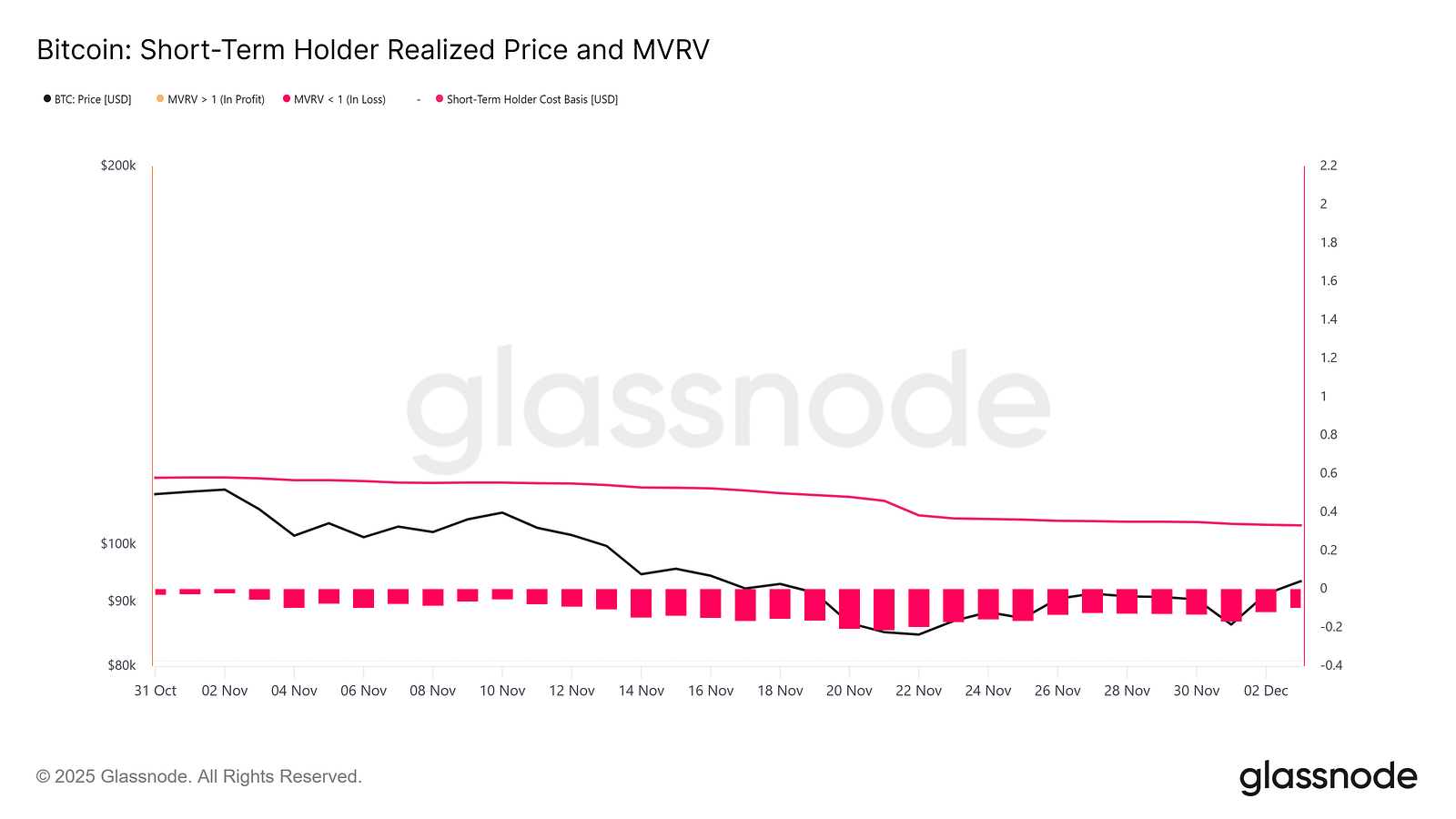

Bitcoin price tumbled by 17.5% MoM on the back of waning investor risk appetite and institutional inflows. As the price failed to sustain $100K, a key level that most short term holders (STH) entered at, most holders are currently unprofitable. Institutional appetite has also weakened with BTC ETFs recording its second worst month since launch with more than $3.48B in outflows. With sentiment pessimistic and liquidity thinning, investors are cautious about catching the falling knife.

Digital asset treasuries which once used to be a major source of supply sink has also receded into the distance as performance across major firms are starting to reveal cracks. At the closing price on 30 November, most BTC DATs have cost price above $90,394, putting them at a loss which could also dampen further appetite to accumulate BTC, at least till they are able to cover their investment cost. Strategy also saw its mNAV dipped below 1 for the first time as higher volatility of the stock led to price plunging harder than the underlying BTC. With the initial euphoria in DATs faded, the uncertain macro environment today highlights the pressing issue that these DATs face when price declines — to sell BTC or not. Under current bearish sentiment, firms are likely to pause further purchases while awaiting for the next catalyst. A decisive rebound in BTC above $100K would offer much relief to these firms, while continued depressed pricing could pressure some of these firms to sell BTC, which some already did to cover their cost of debt and cut losses, or be acquired by larger players who have both capital and execution capability in timing crypto market cycles.

Ethereum and L2s

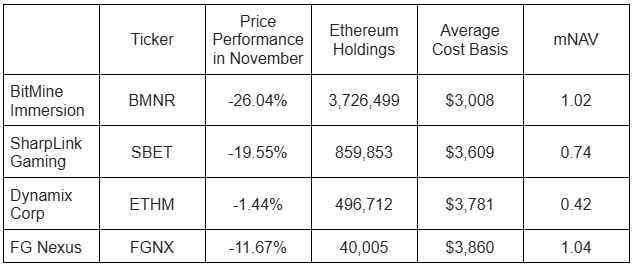

Ethereum price declined by 22.23% MoM in November dragged down by the bearish macro backdrop. Institutional support has also noticeably weakened as ETH ETFs recorded its worst outflows to date, totaling more than $1.4B in redemption. Ethereum treasury companies which previously went on an accumulation spree have been on the sideline in November, with some even reducing their stake such as FG Nexus which sold 10,000 ETH on 20 November to fund their share buyback program. A notable exception was BitMine Immersion which bought the dip, increasing their total holdings to 3,726,499. BitMine engaged in 3 major purchases, adding 110,288, 54,156, and 69,822 ETH on 10th, 17th and 24th November respectively.

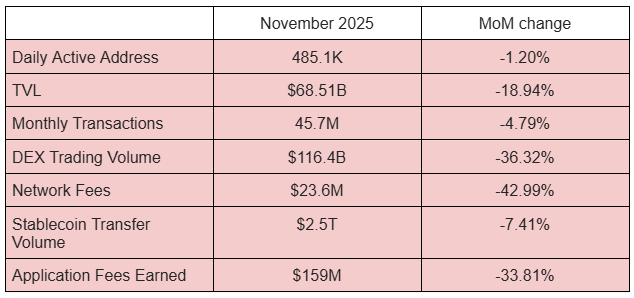

Performance Metrics of Ethereum in November

Evidently, the Ethereum onchain ecosystem was not spared from the pessimistic macro overhang as retail users and investors reduced their exposure. Activity declined across the board with usage metrics falling consequently leading to a significant reduction in network fees and application fees earned.

At the protocol level, developers increased block gas limit to 60M from 45M ahead of the Fusaka Upgrade, thereby increasing block throughput and further lowering transaction fee on Ethereum.

L2 Performance Metrics

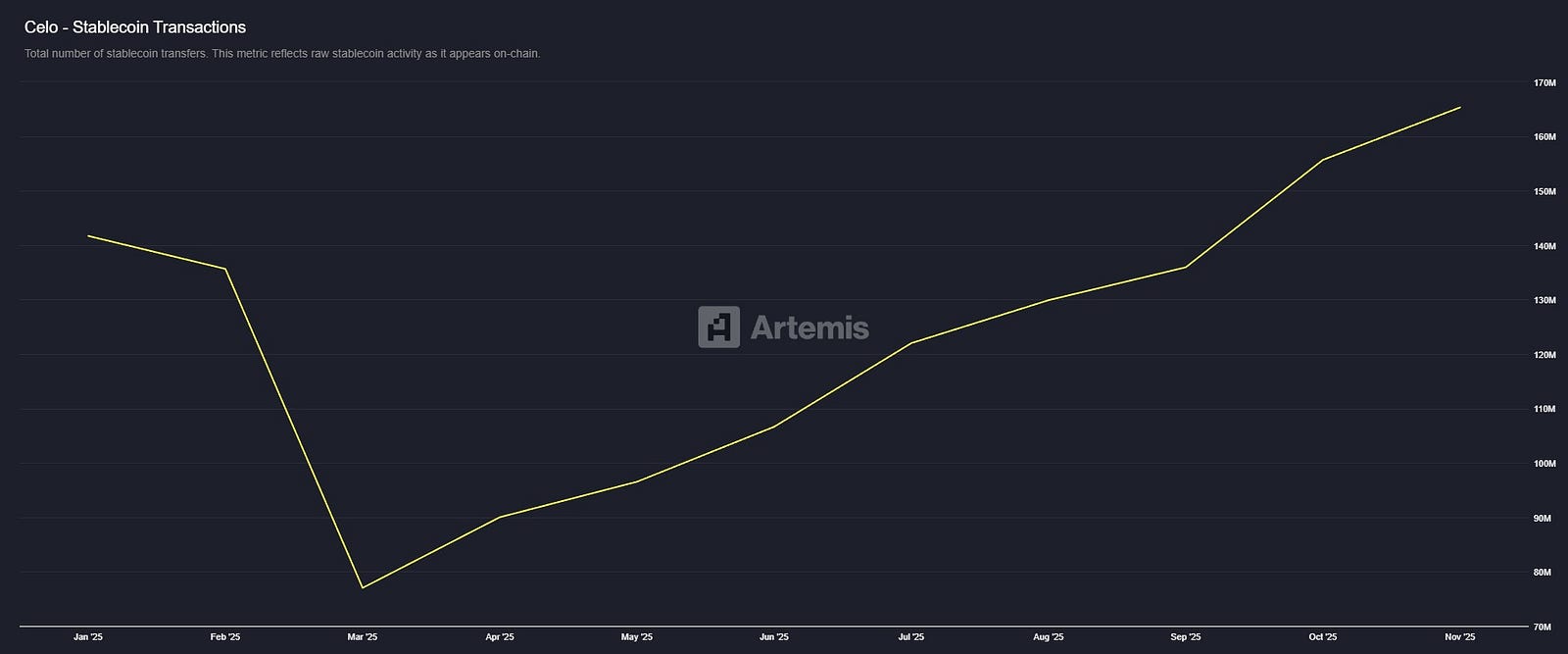

L2s fared worse than Ethereum, with many experiencing more severe price drawdown. Despite high throughput that pushes transaction count higher, most of these transactions are low-fee activity like stablecoin P2P transfers with DEX and Perp DEX activity bearing the brunt in November. A standout performer has been Celo, which continuously grew its daily active users since June, from 497.9K to 742.8K in November. Monthly P2P stablecoin transactions rebounded sharply from March lows to reach 54.8M and overall stablecoin transfers achieved all-time highs. This growth is supported by MiniPay, Celo’s native wallet, which has deepened its collaboration with the Celo Foundation and recently expanded into Latin America. The new “Pay Like a Local” feature enables users to spend stablecoins through familiar local payment rails, allowing merchants to receive direct fiat settlements.

Other notable developments in the Ethereum ecosystem:

Ethereum Foundation introduced the Ethereum Interop Layer that is wallet-centric and built on the ERC-4337 account abstraction principles and the trustless manifesto.

JP Morgan’s tokenized deposits went live on Base.

Arbitrum DAO passed a proposal to transfer 8,500 ETH revenue accrued from its sequencer and timeboost revenue to the Arbitrum Treasury Management Council which generates yields on these stagnant holdings and boost ecosystem support.

Other L1s

Solana

Solana DEX trading volumes contracted sharply in November as leading DEXs reported thinning liquidity thus contributing to lower network fees. Memecoin launchpad, Pump.fun, also cooled for 2 consecutive months underscoring dwindling appetite for high risk memecoins as liquidity concentrates towards blue chip assets. Despite poor onchain metrics in November, Solana continues to make headways into the consumer market as it started shipping 150,000 Solana Seeker phones. The Seeker phone, priced at $500, offers users a built-in onchain experience, with unique seeker ID, non-transferrable genesis token, secure hardware level security that serves as a gateway to the Solana ecosystem from the get go.

On the governance side, another contentious proposal (SIMD-0411) submitted by Helius Labs aims to double the disinflation rate from 15% to 30%. This comes after SIMD-0228 which sought to introduce a dynamic staking schedule based on SOL staked got rejected. By doubling disinflation rate, this could potentially help mitigate sell pressure from the high staking yields but could make staking less attractive and edge out smaller validators. The proposal is still ongoing and we continue to monitor the developments alongside the upcoming Alpenglow Upgrade (expected Q1 2026).

Other notable developments:

SOL Strategies selected to be staking provider for VanEck Solana ETF which currently has $17.2M in AUM through its Orangefin validator.

DeFi Development Corp, a Solana treasury operator, posted $4.6 million in Q3 revenue, an 11.4% organic SOL yield, and $74 million in unrealized gains, supported by its validator network and active on-chain treasury deployment strategies.

TON

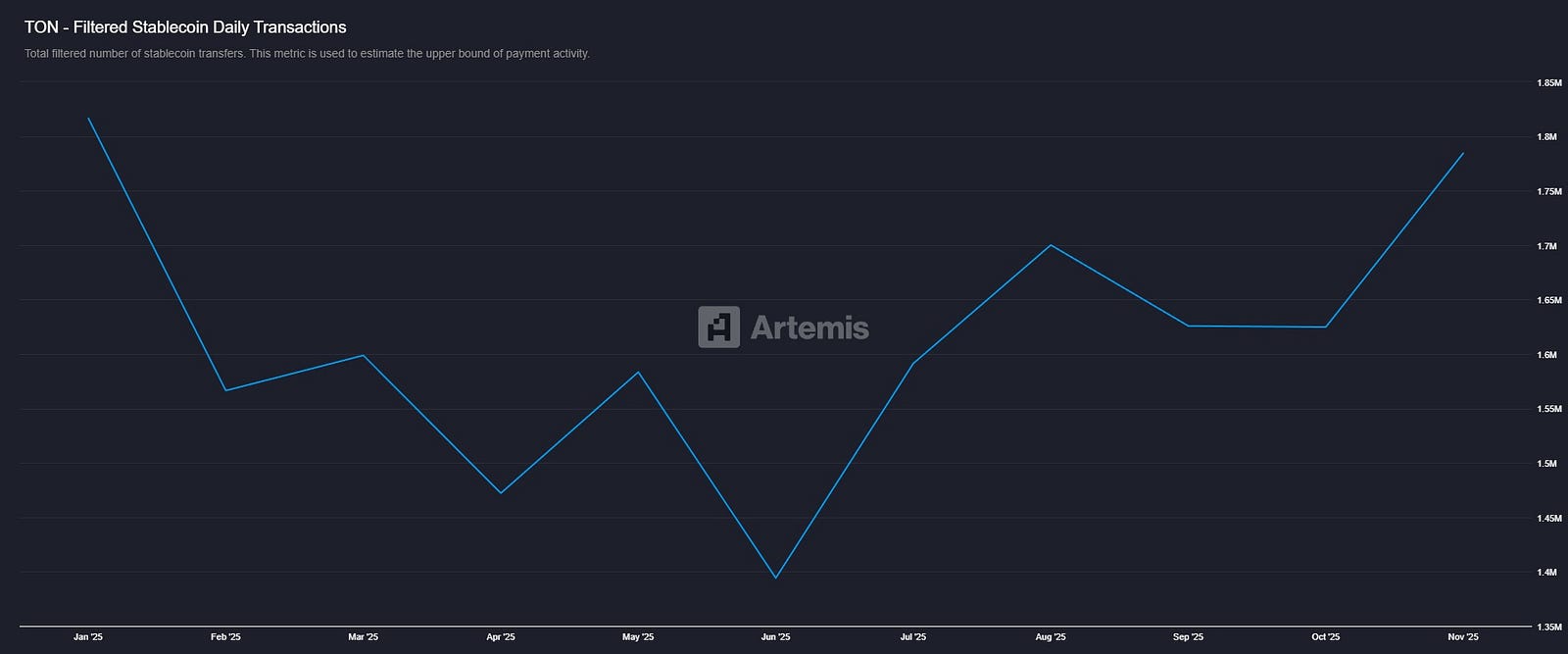

While the network has seen metrics declined across major metrics, a silver lining emerged as its user base is increasingly pivoting from onchain DeFi activities to leveraging the network for fast, low cost, low-value stablecoin transactions. Stablecoin users (MAU — 537K) on the network broke previous records, reaching all-time highs while transaction count also was the second highest on record which could be attributed to its expanded market base after TON Wallet became available in the US in November.

RWA

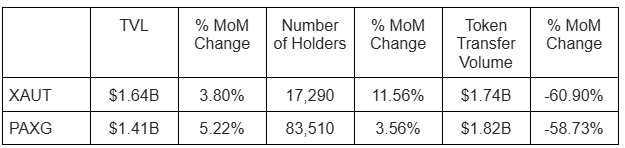

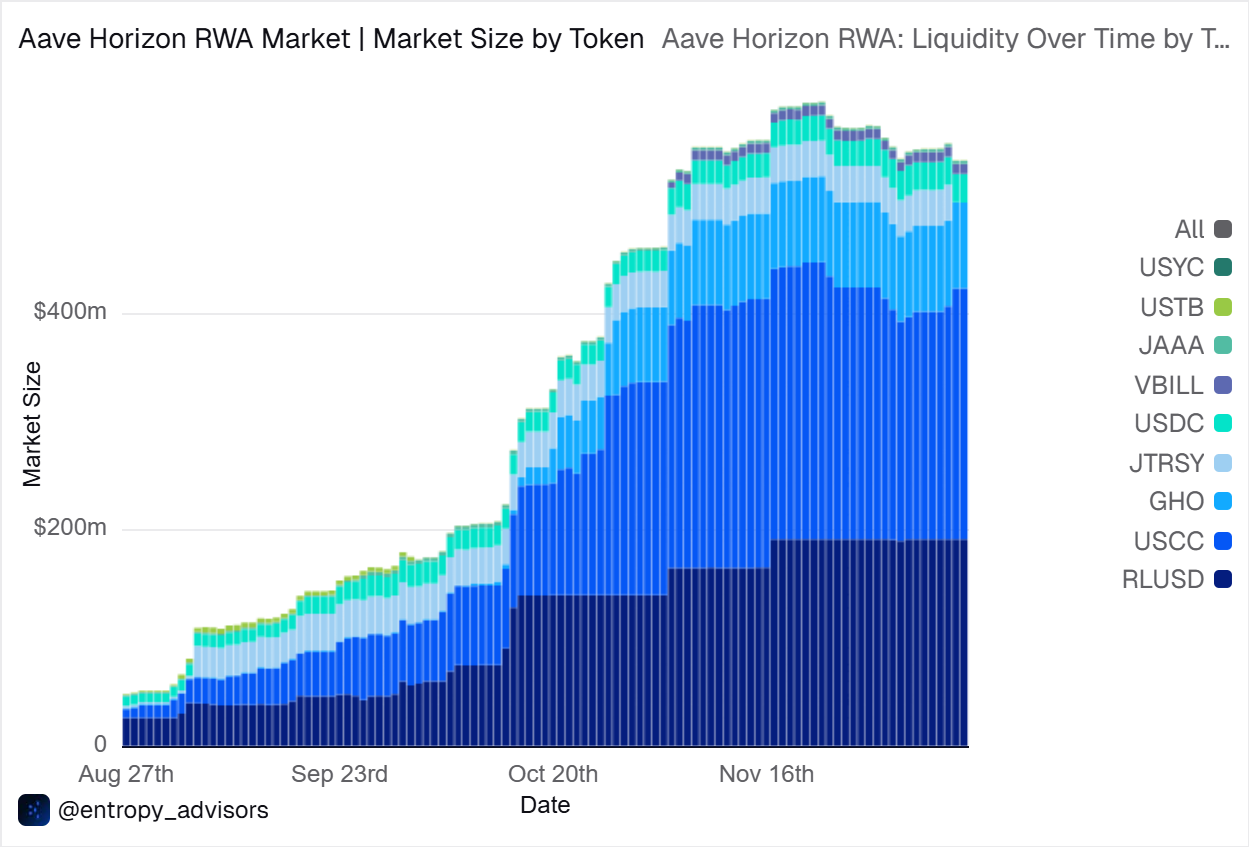

With gold price rising ~5% in November, tokenized commodities have benefitted as well with Tether Gold and Paxos Gold further expanding their AUM and user base, although transfer volume has sharply declined which could be attributed to the increased risk-off sentiment among investors leading them to hold onto their tokenized gold instead of selling/transferring away. Private credit also decoupled from broader market trends by recording growth in its active loans. Aave Horizon expanded its capital beyond $550M with average utilization being ~62% and loans being taken out in USDC, RLUSD, and GHO. Currently, more than 274 unique addresses have also been onboarded onto its platform. Other RWA sectors like tokenized treasuries and tokenized funds fell out of favor along with the broader macro landscape.

Plume Network

Plume Network, now the third largest RWA chain in RWA issuance count, has experienced significant growth this year with RWA TVL increasing from $45.2M in June to $121.1M in November, a 2.6x step up. Asset holders on Plume also eclipsed the total number of holders on Ethereum and Solana combined, underscoring the more retail-focused demographics on the chain. Securitize has also partnered with Plume to distribute its tokenized products on Plume’s nest vaults bringing access to institutional-grade products to the largest RWA community.

BNB Chain

From June to November, BNB increased its RWA TVL substantially from ~$20M to more than $1.6B as its ramped up efforts (RWA incentive campaign in May) to onboard RWA assets. Most notably, BlackRock’s BUIDL expanded to BNB chain in November, bringing more than $500M in TVL alone. Ondo’s tokenized stocks on BNB also saw elevated activity beginning November after Ondo Global Markets entry in late October. Circle’s USYC officially opens up to the ecosystem, enabling USYC to be used across various DeFi use cases like lending, margin trading etc. This native composability drove further demand, cementing USYC lead as the dominant RWA asset on BNB.

Other notable developments:

Kraken acquired Backed Finance.

Hong Kong’s third tokenized green bond received overwhelming interest as the offering got 13x oversubscribed, raising up to HK$10B.

Plume brings 5 RWA yield vaults on Solana with institutional-grade assets from WisdomTree, Hamilton Lane, BlackOpal, and issuers like Securitize and Superstate. Solv Protocol also announced plans to invest up to $10M in Plume’s RWA vaults.

Amundi launched its first tokenized money market fund.

Binance wallet adds tokenized stocks trading feature.

Tether becomes the largest gold holder outside of central banks.

Securitize gets EU approval to operate a regulated trading and settlement system and plans launch of tokenized securities platform on Avalanche in early 2026.

Stablecoins

Amid the flight to safer offchain assets, stablecoin faced heightened headwinds in November. Its total circulating supply wiped off more than $1B, the first monthly decline in 26 months amid broader crypto outflows. Ethena’s USDe alone wiped off more than $2B in supply as Bitcoin and Ethereum price declined, dragging funding rates along. The depeg of stablecoins like deUSD, XUSD, USDX further aggravated negative sentiments towards unmanaged leverage yields and operational failures. Despite the broader risk-off sentiment sending ripples across Ethena’s ecosystem, the protocol remained overcollateralized and still benefitted from having positive funding rates on most days, underscoring the robustness of the protocol under periods of stress. Another key player under stress was Tether, which got downgraded by S&P Global to the lowest level citing an increase in high risk assets and inadequate disclosures. Notable gainers in November include Circle’s USYC and Paypal’s PYUSD which grew 40.35% and 39.29% MoM respectively. Overall, adjusted stablecoin transaction volume declined from October’s peak to $2.8T, a drop of 22.22% MoM. While larger transactions seem to have receded to risk-off assets offchain, the number of active stablecoin addresses remains near all-time highs, highlighting the increasing prevalence of stablecoin in retail users’ daily lives.

Other notable developments:

Exodus wallet acquired W3C Corp to expand the crypto payment stack.

QCAD became the first compliant stablecoin in Canada.

Naver to launch stablecoin wallet with Hashed and BDAN.

BNPL firm Klarna announced USD stablecoin, KlarnaUSD, on upcoming Tempo, bringing stablecoin access to its 114M users.

Tether ceased EURT redemptions across all supported blockchains.

Revolut enables in-app USDC and USDT transfers on Polygon.

Alibaba to use JP Morgan blockchain for tokenized dollar and euro payments.

Grab and StraitsX signed an MOU to develop web3 wallet and stablecoin-based settlement. StraitsX will offer support to develop web3 wallet integrated with web2 payment rails and web3 settlement. This enables merchants to accept stablecoins and users to transact with StraitsX XSGD and XUSD.

Paxos Labs announced USDG0, with initial network integration with Hyperliquid, Plume, Aptos.

Circle announced StableFX and Partner Stablecoin to build onchain FX infrastructure.

Paystand acquired stablecoin network Bitwage.

South Korean bank NongHyup Bank pilots stablecoin-led tax refunds on Avax.

Ripple Labs is partnering with Mastercard to offer RLUSD credit card settlement on XRP ledger.

Notable M&A/Fundraising and Portfolio Updates

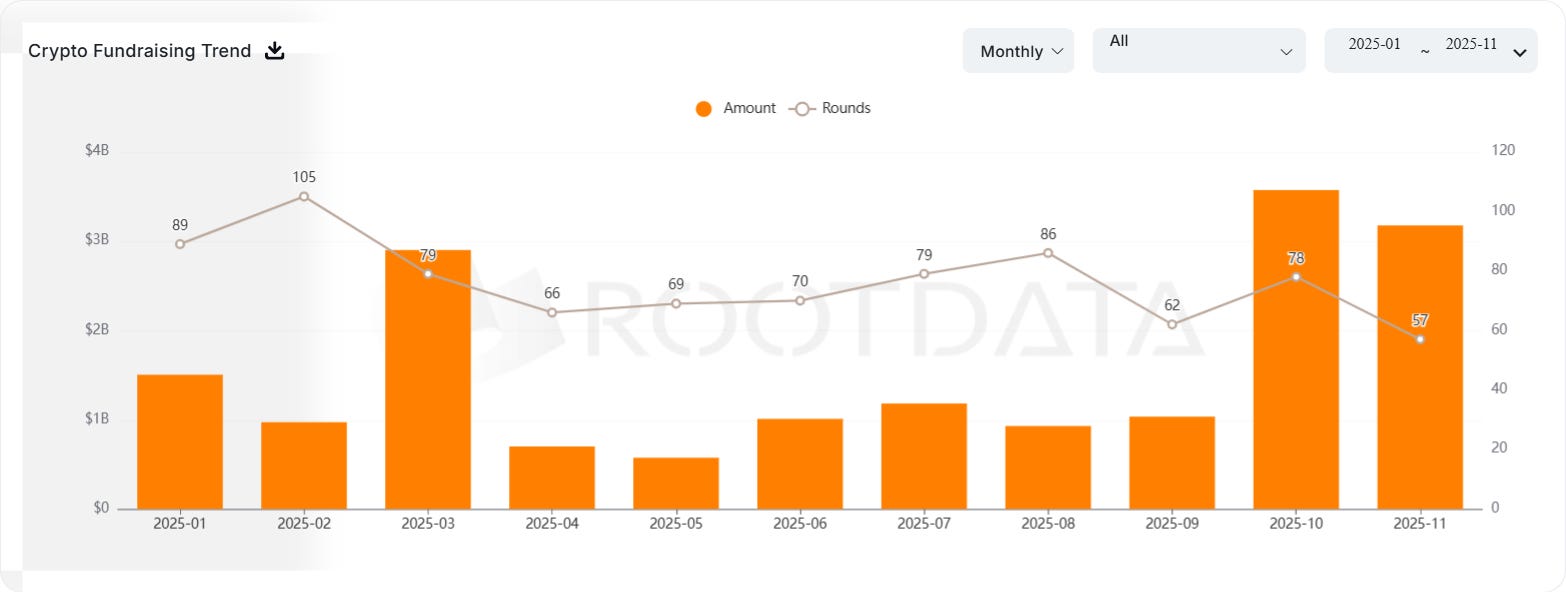

Although fundraising activity declined in November, deal value remained near all-time high this year, second to October’s peak. However, deal count reached its lowest level, underscoring the dominance of late stage deals and funding preference for more mature startups.

Portfolio Highlights

Sign introduced the Sign L2 stack built on BNB, enabling nations to deploy compliant stablecoin contracts.

Plume is onboarding Securitize to offer institutional-grade assets to Nest protocol.

Kaito launched a verifiable mindshare market on Polymarket, partnering with Brevis and Eigencloud.

Huma announced it has crossed $8b in PayFi transaction volume, expecting $20m ARR.

Space and Time launched Space and Time v2. With the latest mainnet upgrade, institutions can now use SXT to secure offchain financial datasets and power more sophisticated asset tokenization onchain.

AEON’s BNB x402 V2 SDK and Facilitator Service is now fully live.

Questflow launched Daydreams, an x402 agent facilitator, processing around 100k+ in transactions a day.

Perle Labs beta is now live.